Why does the Cour des Comptes audit international institutions?

The role of the Cour des Comptes is to ensure the proper use of public funds, in accordance with article 15 of the Declaration of the Rights of Man and of the Citizen: "Society has the right to hold any public official accountable for his administration". In this context, and given that international institutions are the focus of many French contributions (see the Court's report on the financing of France's multilateral actions) and, more broadly, of contributions from all member states, it is important to ensure that these funds are used properly.

Performance and financial audits are carried out on many international institutions. Foreign supreme audit institutions do the same. These missions, which are carried out in complete independence, contribute to France's influence, as well as strengthening the Court's technical expertise. They are also positive for the experience of the Court's staff who take part in them and are confronted, during their missions, with other ways of working and other international standards (Intosai principles and Issai standards, but also Ipsas standards).

Performance and financial audits are carried out on many international institutions. Foreign supreme audit institutions do the same. These missions, which are carried out in complete independence, contribute to France's influence, as well as strengthening the Court's technical expertise. They are also positive for the experience of the Court's staff who take part in them and are confronted, during their missions, with other ways of working and other international standards (Intosai principles and Issai standards, but also Ipsas standards).

Current mandates

The First President of the Cour des Comptes is currently the external auditor of four international organizations: the World Trade Organization (WTO), as of 2020, the United Nations (UN), as of 2022, and the International Organization for Migration (IOM), as of fiscal year 2025, and the International Civil Aviation Organization (ICAO), as of fiscal year 2026.

With regard to the UN's audit mandate, the Court's portfolio comprises four pillars of strategic importance:

1. Peacekeeping operations

2. Development (in particular the United Nations Development Programme, UNDP)

3. Human rights and refugees (including the Office of the United Nations High Commissioner for Refugees, UNHCR)

4. Climate conventions.

France is a member of the UN Board of Auditors until 2028, alongside China and Brazil, and in 2024 chaired the Panel of External Auditors, which brings together the twelve external auditors of the United Nations, specialized agencies and the International Atomic Energy Agency (IAEA).

In addition to these audit missions, the Court makes magistrates available to European organizations such as Arte, the Franco-German University, the European Peace Facility (EPF), the Organization for Joint Armament Cooperation (OCCAr) and the European Organization for Nuclear Research (CERN).

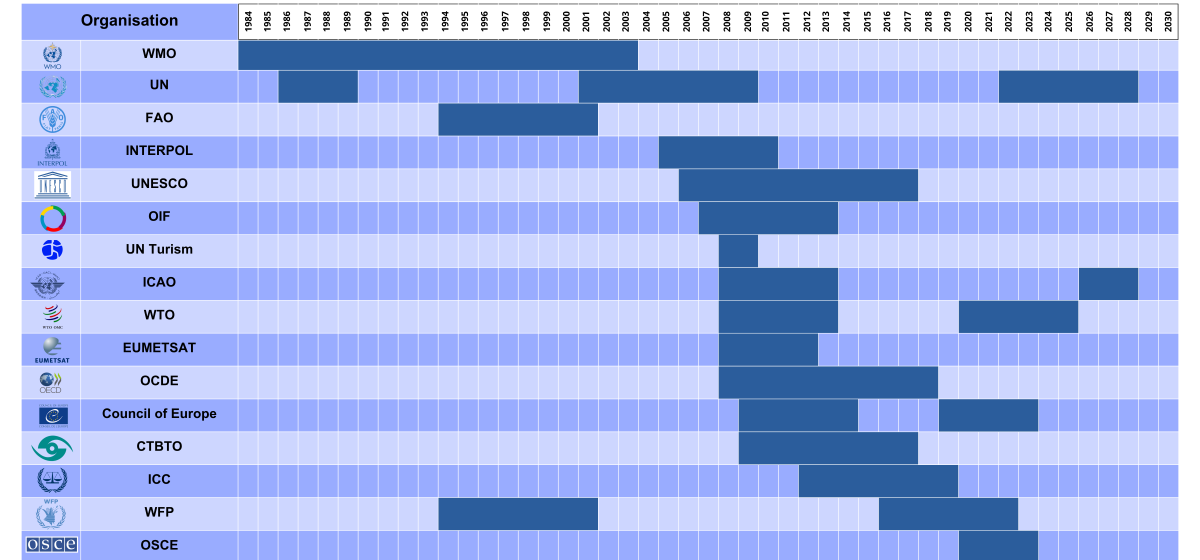

History of mandates held

Over the past forty years, the Court has carried out continuous external audits of at least one UN-related organization. : Here is the list of international organizations that have entrusted the Court of Auditors with an external audit mandate at least once:

• United Nations (UN)

• World Meteorological Organization (WMO)

• Food and Agriculture Organization of the United Nations (FAO)

• Interpol

• UNESCO

• International Organization of La Francophonie (OIF)

• World Tourism Organization

• International Civil Aviation Organization (ICAO)

• World Trade Organization (WTO)

• European Organization for the Exploitation of Meteorological Satellites (EUMETSAT)

• Organization for Economic Cooperation and Development (OECD)

• Council of Europe

• Comprehensive Nuclear-Test-Ban Treaty Organization (CTBTO)

• International Criminal Court (ICC)

• World Food Programme (WFP)

• Organization for Security and Co-operation in Europe (OSCE)

• International Organization for Migration (IOM)

The external audit method

The missions entrusted to the Court's teams and the audit directors who head them consist in carrying out three types of audit: financial, compliance and performance. The financial statements for each accounting period are audited, with the aim of enabling the First President to issue an opinion on the accounts of each organization (the equivalent of the certification of the State's accounts). At the same time, the Court's teams examine the management of these organizations through performance and compliance audits. The financial and performance audits involve travel, or even a permanent presence, both at the United Nations headquarters in New York and at the Palais des Nations in Geneva, and in the field, in the countries where the international organizations operate. In addition to headquarters, the Court carries out budget and compliance audits on the country offices and activities of the various institutions. The results of these audits are presented each year by the First President to the governing bodies of the audited institutions; most of them publish these reports.

In its audits, the Court systematically applies five principles:

1. Risk-based approach

2. Collaboration with the internal audit bodies of the audited institutions

3. Audit traceability

4. Verification and quality control

5. Follow-up of recommendations issued by the Cour des comptes

The Court bases all its financial and performance audits, as well as their planning, on a strategic approach based on three essential objectives:

1. In-depth understanding of the organization

2. Evaluation of its internal control system

3. Identification of key risks

At the end of each audit, the institution's management may raise justified objections to the facts and data presented in the Court's draft reports. After corrections have been made and management's formal observations considered, the Court submits the final reports and follow-up recommendations to the audited organization's governing bodies.

Find out more about the Court's external audit reports

You can consult the audit UN agencies reports or the performance and financial audit of the WTO